A few years ago, “experiential marketing” was a line item most Indian brand managers treated like a luxury. Something you did if there was budget left after the festive campaign. Something the cool D2C brands did at pop-ups. Not something that sat at the centre of a quarterly plan.

That position has shifted considerably. A joint report by EY-Parthenon and BookMyShow, released in March 2026, found that 78% of Indian consumers now prefer spending on experiences over products. More than half of surveyed brands ran experiential activations in the past year. And 88% of those that invested in experiential marketing plan to continue in a more structured, intentional way. (Source: EY-Parthenon + BookMyShow, ‘Beyond Attention. Into Immersion’, March 2026)

That last phrase is the one worth sitting with. More structured. More intentional. Because the trend is not simply that brands are doing more events or building more activation booths. It is that the underlying logic of how Indian brands think about promotions, rewards, and consumer engagement is changing in a fundamental way. And 2026 is the year that shift is becoming visible in planning cycles, budget allocations, and on-ground execution.

This blog is an attempt to map what is actually changing, why it is changing, and what it means for brand managers, category heads, and trade marketing teams who are building their next cycle of promotional activity.

Before we get into this, here are a few relevant resources from Buyerr:

- Consumer Promotions for FMCG and Retail Brands

- Thematic and Seasonal Campaign Solutions

- Experiential Rewards

You can also explore:

What we’ll cover:

- The Market Context: Where Indian Retail Promotions Stand in 2026

- Trend 1: Experiential Marketing Is No Longer Optional

- Trend 2: Promotions and Loyalty Are Converging Into One Engine

- Trend 3: Instant Gratification Is Now the Baseline, Not the Bonus

- Trend 4: Phygital Is Moving from Concept to Execution

- Trend 5: First-Party Data Is Becoming Promotions’ Most Valuable Output

- Trend 6: Tier 2 and Tier 3 India Is the New Experiential Frontier

- What Brands Often Get Wrong Reading These Trends

- A Quick-Decision Framework for 2026 Promotion Planning

1. The Market Context: Where Indian Retail Promotion Trends Stand in 2026

India’s retail and FMCG landscape heading into 2026 is defined by a few simultaneous pressures that are forcing a rethink of how promotions are designed.

On the demand side, consumers are more informed, more fragmented across channels, and more willing to switch than at any point in the recent past. FMCG volumes surged nearly 14% in mid-2025, reflecting a market that is growing but also one where competition for shelf space, consumer attention, and repeat purchase is intensifying. India’s ad market is projected to reach close to INR 2 trillion in 2026, growing approximately 10% annually. (Source: WPP ‘This Year, Next Year’ forecast, via ClickUp, December 2025)

On the supply side, margins are tighter. The era of running blanket discounts as a primary promotional tool is coming under pressure from finance teams who want to see promotions evaluated like investments. As Buyerr’s own 2026 trend analysis noted, brand leadership is increasingly asking not “did we spend the scheme budget?” but “did repeat purchase improve? Did churn drop? Did distributor offtake increase?”

And running through both of these realities is a structural shift in consumer behaviour: the growing primacy of experience as a purchase motivator. More than 70% of Indian shoppers now favour active engagement over traditional shopping, driven primarily by millennials, Gen Z, and Gen Alpha. (Source: CPM India, Indian Retail and FMCG Sector Trends, 2026)

These three pressures together are reshaping the promotional toolkit. What they add up to is a market where reaching a consumer is no longer sufficient. Engaging them is the new minimum.

2. Trend 1: Experiential Marketing Is No Longer Optional

The headline number from the EY-Parthenon and BookMyShow report deserves to be read carefully. India’s live events market reached an estimated INR 13,000 crore in 2025 and that figure was projected to grow toward INR 17,000 crore by the end of 2025 based on annualised estimates. Live events were the single fastest-growing segment in India’s media and entertainment industry, recording 44% growth in 2025 per the FICCI-EY Media & Entertainment Report 2026.

This is not a cultural footnote. It is a signal about where consumer attention is genuinely going and where brands need to follow it.

The commercial case for experiential investment is also strengthening. The EY-BookMyShow research surveyed 7,450 attendees across major events including Lollapalooza India, Ed Sheeran, and Guns N’ Roses concerts. 59% of attendees recalled brands they interacted with on-ground. 55% reported higher purchase intent after engaging with a brand at the event. And notably, 63% said the brand activation enhanced their overall event experience rather than distracting from it.

The last data point is the one that changes the framing entirely. Consumers are not tolerating brand presence at experiences. They are welcoming it when it is done with design intent rather than just logo placement. There is a meaningful difference between a brand that sponsors an event and puts up banners, and a brand that designs an experience within an experience. The former is visibility. The latter is memory.

Among brands that increased their experiential marketing spend over the past three years, 44% reported revenue growth of up to 30%. Globally, experiential marketing spend is projected to reach USD 130 billion by 2025, growing at 10.5% annually, with 74% of Fortune 1000 marketers planning to increase their investments in experiential formats. (Source: Adgully, March 2026)

For Indian brand managers, the practical implication is this: if experiential marketing has not yet appeared meaningfully in your 2026 activation calendar, the question is not whether to start but how to start well.

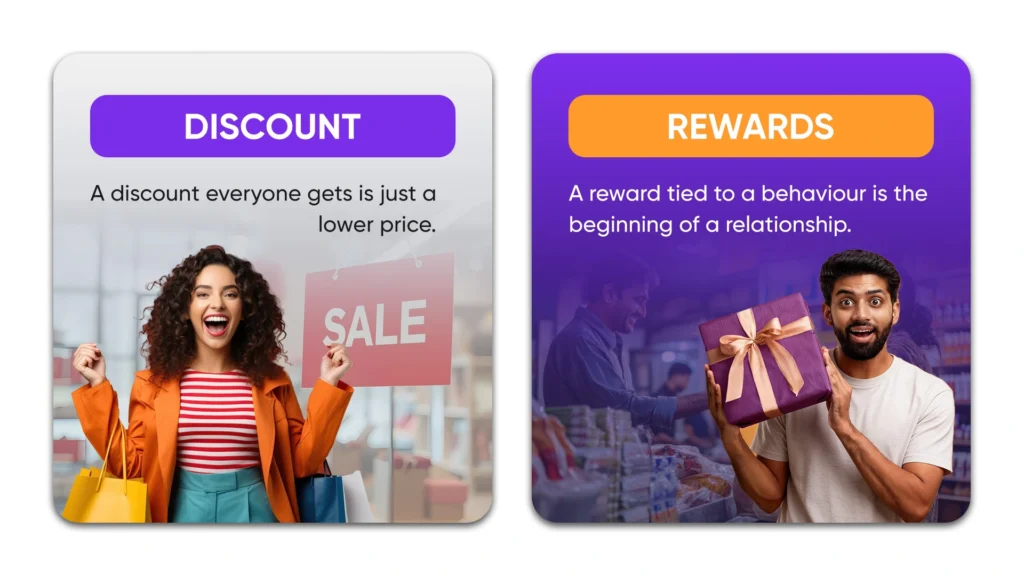

3. Trend 2: Promotions and Loyalty Are Converging Into One Engine

For most of the past decade, promotions and loyalty programs sat in separate boxes within a brand’s commercial plan. Promotions were short-term, a scheme to drive volume this quarter. Loyalty was long-term, a program to keep the consumer coming back. Different metrics, different budgets, different teams.

In 2026, that separation is breaking down. And it is breaking down in a commercially interesting direction.

Brands are increasingly designing promotions that are also loyalty-building mechanisms. Instead of a flat 15% festive discount visible to everyone, the smarter architecture looks like:

“Register and unlock 15%.”

“Scan to access cashback.”

“Members get early access pricing.”

The discount has not disappeared. But it is now tied to a behaviour: registration, scanning, repeat purchase – that gives the brand something back in return. Data, engagement, channel visibility.

This shift is particularly visible in FMCG and retail categories where purchase frequency is high. When a consumer buys the same category product every two to three weeks, every transaction is an opportunity to deepen the relationship rather than simply fulfil the order. Brands that are building this logic into their promotion mechanics are finding that the same spend goes further, because each promotional interaction is also a loyalty touchpoint.

The data from the Indian loyalty market supports the direction of travel. According to a study, India’s loyalty program market is expected to surge from USD 4.3 billion in 2025 to over USD 17 billion by 2035, at a compound growth rate that reflects both increasing consumer participation and increasing brand investment.

The architecture of consumer loyalty solutions is evolving alongside this. Unified loyalty IDs incorporating mobile numbers, UPI IDs, and WhatsApp profiles are enabling seamless reward delivery across channels, online and offline, for the first time at a meaningful scale. A consumer who buys at a kirana and at a modern trade outlet and through quick commerce can now be recognised as the same person, and their loyalty can be rewarded consistently across all three. This is infrastructure that changes what is possible.

4. Trend 3: Instant Gratification Is Now the Baseline, Not the Bonus

Consider two brands both running a cashback promotion.

Brand A: upload the invoice, wait 21 days, track claim status.

Brand B: scan QR code, receive UPI cashback within minutes.

The reward amount is the same. The emotional experience is not. And in 2026, the gap between those two experiences is widening, not narrowing.

Indian consumers in 2026 are not asking for better rewards. They are asking for faster ones. The shift is from “what will I get?” to “when will I get it?”. And that timing is becoming a brand trust signal.

The UPI infrastructure has made instant digital disbursement structurally possible at scale. India’s total digital transaction value is projected to reach USD 1 trillion by 2026, up from USD 300 billion in 2021. (Source: IBEF, Indian FMCG Industry Analysis) With UPI deeply embedded in daily purchase behaviour, the expectation of instant, friction-free reward delivery has crossed from early adopter preference to mass-market baseline.

This has practical implications for how cashback and digital coupon mechanics are designed. Programs that still rely on manual claim submission, delayed credit timelines, or complicated eligibility documentation are not just operationally inconvenient; they are actively eroding consumer trust in the brand running them. Brightspot Incentives research has documented that when participants must manually submit claim forms, take rates drop to between 20% and 40%. When claims are auto-validated, engagement is meaningfully higher.

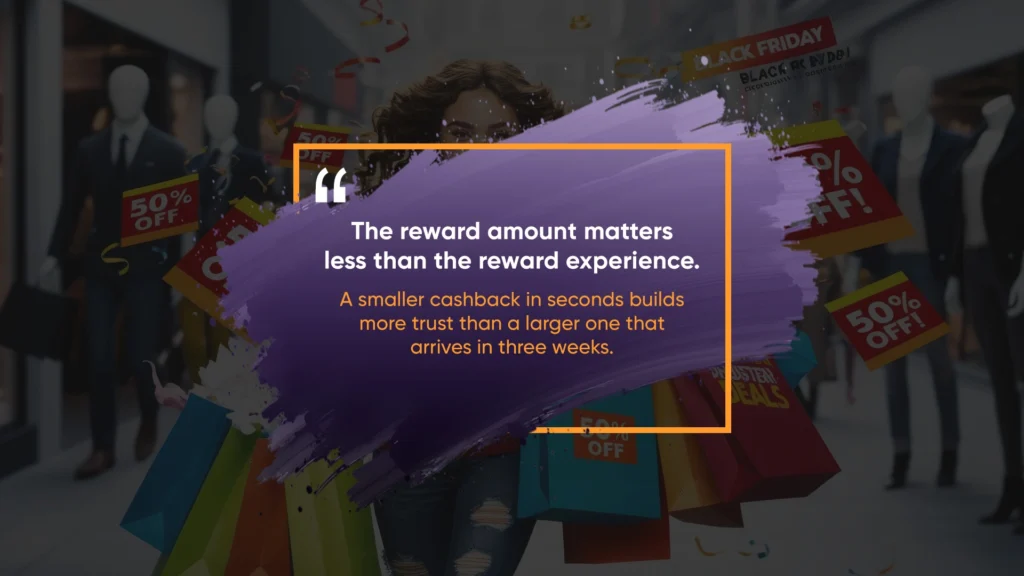

The implication for brand managers and trade marketing teams is direct. When designing a promotion for 2026, the reward amount matters less than the reward experience.

A smaller cashback that arrives in seconds builds more trust than a larger cashback that arrives in three weeks.

Building this expectation of immediacy into promotion architecture is now the price of entry for a program that will actually achieve its participation targets.

5. Trend 4: Phygital Is Moving from Concept to Execution

Phygital: the blending of physical and digital consumer experiences, has been discussed as a trend for several years. In 2026, the distinction is that it is moving from strategy decks into actual execution, at a scale that is starting to generate measurable results.

Over 250 million Indians engaged with AR filters in 2025, a base that is continuing to grow as smartphone penetration deepens and 5G expands access. Brands are now deploying AR filters on packaging, NFC-enabled retail touchpoints, scan-to-win QR codes, and interactive in-store displays that connect the physical purchase moment to a digital reward or experience.

The Britannia Marketing team articulated this direction clearly in early 2026: “Consumers are actively seeking a phygital experience of getting connected online for an offline experience, which will result in stronger communities being built for sustained engagement.” (Source: Social Samosa, FMCG Marketing Trends India 2026, January 2026) The framing, online for an offline experience, captures the direction of travel. Digital is not replacing the physical retail or event moment. It is enriching it, extending it, and making it trackable.

For FMCG brands specifically, retail and on-pack promotions are where this phygital shift is most practically actionable. A QR code on a pack that links to an instant cashback, a gamified contest, or a personalised recipe suggestion is a phygital touchpoint that costs relatively little to execute but meaningfully changes the consumer’s interaction with the product at the moment of purchase or consumption. It also creates a data trail. The consumer who scans the pack, claims the reward, and returns to buy again is now identifiable, trackable, and market-able to in a way that the anonymous purchase never was.

The more sophisticated version of this is what Fortune Edible Oils outlined as its 2026 direction: transforming from a brand that “participates in culture” to one that “powers everyday cultural discovery, cooking inspiration, and community connection, both online and offline.” (Source: Social Samosa, FMCG Marketing Trends India 2026, January 2026) That is a phygital vision at the brand level, not just a campaign mechanic.

6. Trend 5: First-Party Data Is Becoming Promotions’ Most Valuable Output

Here is a shift that is happening quietly inside most marketing functions, but has significant implications for how promotions are designed and evaluated.

As third-party cookies become obsolete and privacy regulations tighten, brands are realising that consumer promotions, on-pack activations, cashback programs, scan-to-win mechanics, loyalty enrollments are among the highest-quality first-party data collection opportunities available to them. A consumer who scans a QR code, submits a claim, selects a reward preference, and completes a purchase has generated a rich data signal: who they are, what they buy, how they engage with rewards, and what motivates their next purchase decision.

Most brands are still treating this data as a byproduct of the promotion. The emerging best practice is to treat it as a primary output and to design the promotion architecture accordingly. This means building consent-based data capture into the claim flow, linking promotion data to CRM systems, and using the resulting consumer profiles to personalise subsequent communications and offers.

The commercial impact of this data-first approach is not speculative. According to data, AI-driven personalised offers matching consumer preferences have been shown to boost program effectiveness by up to 47%. Personalised experiences in retail generally generate up to 15% revenue uplift and improve marketing efficiency by 30%.

First-party data and consumer insights platforms built specifically for FMCG and retail contexts are what make this operationally achievable. The infrastructure now exists to capture, structure, and act on consumer data generated through promotional interactions at a scale and cost that was not practical five years ago. Brands that build this capability in 2026 are creating a compounding advantage: each promotion teaches them more about their consumers, which makes the next promotion more effective, which generates better data, and so on.

7. Trend 6: Tier 2 and Tier 3 India Is the New Experiential Frontier

One of the most important and most underreported aspects of the experiential marketing shift in India is where the growth is coming from geographically.

The EY-Parthenon report noted that over 10 lakh people traveled for live events in the last two years, representing audiences from nearly 1,200 cities across India. This is not a Mumbai-Delhi-Bangalore story. Navratri now spans over 2,000 organised events across cities. Holi music events in mid-sized cities are drawing up to 50,000 attendees. (Source: EY India, Why Brands Are Turning to Experiential Marketing, April 2026)

This geographic expansion of experiential consumption is commercially significant for several reasons. Consumers in cities like Indore, Jaipur, Kochi, and Lucknow have rising disposable incomes and a genuine appetite for brand experiences, but far less competition from other brands for their attention at events. A brand activation in Lucknow generates far more relative impact than the same activation in a saturated Delhi mall environment.

Parle’s marketing team noted that digital now accounts for approximately 20–25% of their total spend, with the remaining majority allocated to physical and on-ground activation across a geographically diverse footprint. (Source: Social Samosa, FMCG Marketing Trends India 2026, January 2026) The regional language dimension compounds this: 76% of online shoppers prefer buying in their native language, and 40% avoid platforms that do not offer it. Experiential activations in Tier 2 and Tier 3 cities that speak in the local cultural and linguistic register are more effective, not less, because they meet consumers where they genuinely are rather than where the campaign assumes they are. (Source: StartUs Insights, Consumer Behavior Trends 2026)

Gamified promotions and contests designed for regional rollout, with vernacular copy, locally relevant rewards, and phygital mechanics that work on mid-range smartphones, are becoming a critical capability for brands that want to capture this opportunity.

8. Where to Start: A Prioritisation Guide for 2026

Six trends in one planning cycle is too many to act on simultaneously. The question most brand heads and category managers are actually sitting with is not “which of these are real?” – most of them are. It is “Given our brand’s current position, where do we focus first?”

A useful way to think about prioritisation is by separating what builds immediate commercial return from what builds long-term capability. Both matter, but they are funded differently, measured differently, and require different internal conversations to get approved.

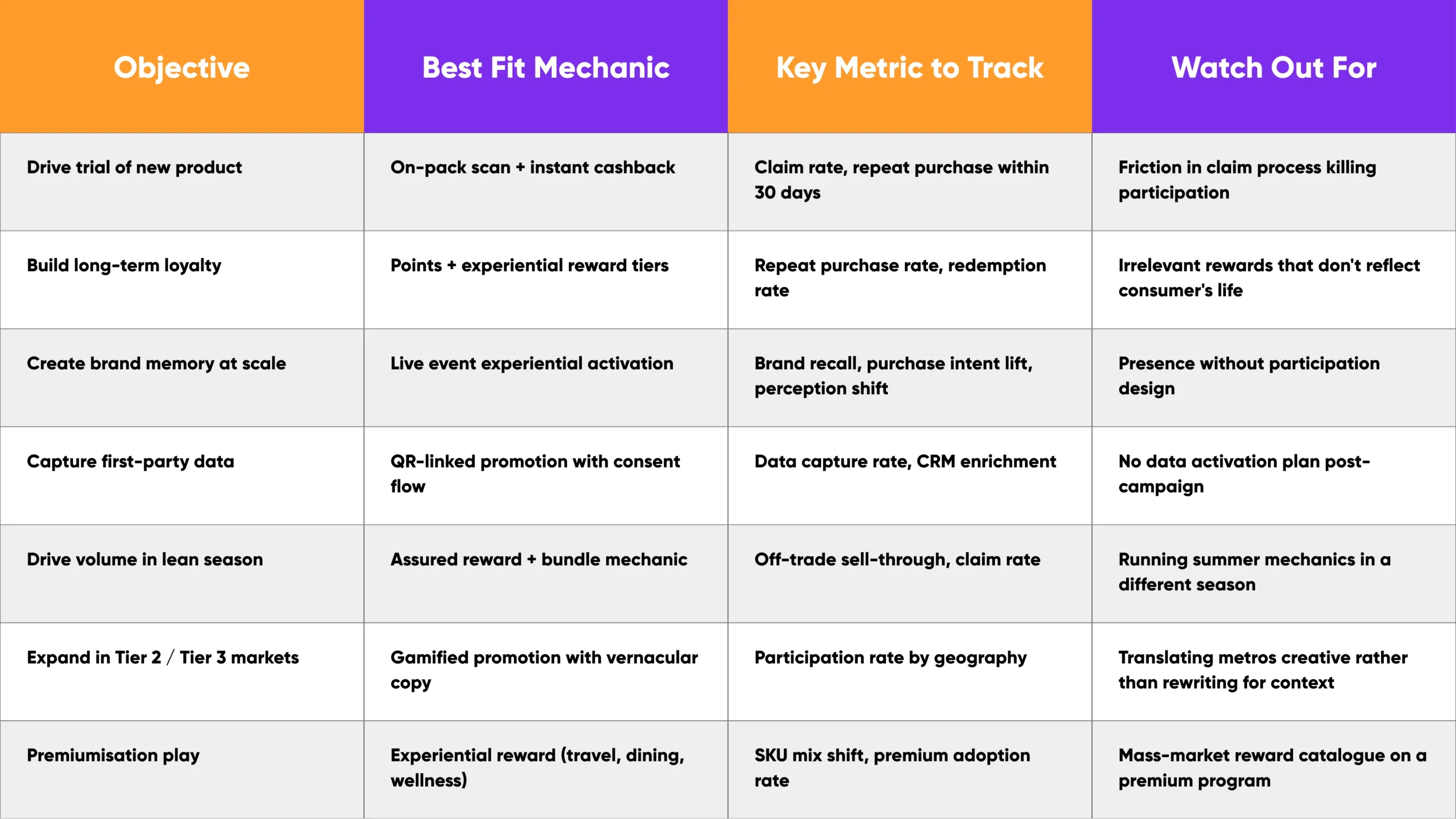

If your most pressing problem is volume and conversion in the next two quarters, the highest-return starting point is Trend 3: instant gratification mechanics. Redesigning your cashback or on-pack promotion to deliver rewards within minutes rather than weeks is a low-infrastructure change with a measurable impact on claim rates and repeat purchase. It does not require a new agency, a new platform, or a new creative direction. It requires a design decision and an execution partner who can make it technically real.

If your most pressing problem is consumer retention and reducing churn, Trend 2: the convergence of promotions and loyalty is where to invest attention. Specifically, the question is whether your next promotional campaign is also enrolling consumers into a loyalty architecture or simply rewarding a one-time transaction. The brands building durable retention in 2026 are the ones making every promotional interaction a reason for the consumer to identify themselves and stay connected.

If your most pressing problem is brand relevance and cultural connection, Trend 1: experiential marketing is the conversation to have. The EY-BookMyShow data is clear enough to take to a budget committee: 55% purchase intent lift, 59% brand recall, and 44% of brands that increased experiential spend reporting revenue growth of up to 30%. The question is not whether to invest in experiential. It is whether to start with a large-format live event activation, a smaller phygital on-pack mechanic, or a regional experiential rollout in Tier 2 cities. All three are legitimate starting points depending on budget, timeline, and geographic footprint.

If your most pressing problem is data, specifically the erosion of third-party data and the need to build owned consumer intelligence, Trend 5 is where to start, and the practical entry point is simpler than it sounds. Add a consent-based data capture flow to a promotion you are already running. Link the claim data to your CRM. Build the first-party profile from there. The infrastructure investment is modest. The compounding return over 12 to 18 months is not.

Think about it this way – these six trends are not six separate workstreams. They are six dimensions of a single direction: toward more intentional, more measurable, more consumer-centric promotional design. A brand that starts with instant gratification mechanics (Trend 3) is also building the infrastructure for first-party data capture (Trend 5). A brand that invests in Tier 2 experiential activations (Trend 6) is also building cultural relevance (Trend 1) in markets where competitors are not yet paying attention. The entry points are different. The destination is the same.

9. A Quick-Decision Framework for 2026 Promotion Planning

The fast decision logic for 2026:

- If the goal is trial → design for instant reward at the point of first purchase

- If the goal is retention → merge promotions into your loyalty architecture

- If the goal is brand memory → invest in participation, not just presence

- If the goal is data → build data capture into the mechanic, not as an afterthought

- If the goal is geographic expansion → design for the local context, not the national template

In Closing – Retail Promotion Trends

The word “trend” can make things feel further away than they are. These are not directions that will matter in 2028. They are decisions that brand managers are making right now, in 2026 planning cycles, about where promotion budgets go and how activation calendars are built.

The underlying shift is not difficult to describe. Indian consumers are moving toward experience, toward immediacy, toward relevance. They are engaging with brands they find worth engaging with, and quietly disengaging from everything else. The promotional tools that worked in 2020 still exist. But their relative effectiveness is declining, and the tools that are working in 2026: experiential activations, instant reward mechanics, phygital touchpoints, loyalty-integrated promotions, are doing so because they meet consumers where behaviour has actually moved.

The brands most likely to come out ahead are not necessarily the ones with the largest promotional budgets. They are the ones that are designing with intent, measuring what actually matters, and building capabilities now that compound over time.

If you found this useful, these related reads may be worth your time:

- How to Plan a High-Impact Consumer Promotion Campaign in India

- Gamification in Loyalty and Promotions: What Works?

- Experiential Rewards: Strategies to Create High-Impact Customer Experiences

- How Promotion ROI Analytics Helps Boost Your Campaign Performance

- In-Store Activation Ideas That Drive Footfall

If you are looking to build promotions that are built for how Indian consumers actually behave in 2026: instant rewards, phygital mechanics, experiential formats, and first-party data capture, explore Buyerr’s consumer promotion solutions or get in touch directly to discuss your 2026 activation plan.

To explore more frameworks, write to us at [email protected] or follow our updates on LinkedIn.